Social Security is an important part of most people’s retirement planning across the country. Some 70 million American workers are receiving benefits through the program. For many of those, Social Security are the majority of their retirement benefits. One of the most critical retirement decisions that one can make is when to apply for and start receiving Social Security. A number of Social Security calculators and other tools have been developed which will help you determine the best time to start receiving payments as well as what you might be entitled to. The calculators, while giving you some important things to think about, are no replacement to the official calculations done by the SSA at the time of retirement.

Below is a list of 7 of the best Social Security calculators you may want to use:

- SSA Retirement Estimator

- mySocialSecurity Retirement Calculator

- SSA Online Benefits Calculator

- CFPB Planning for Retirement Tool

- Social Security Benefits Calculator

- Social Security Calculator

- SSA Life Expectancy Calculator

These calculators can go a long way toward helping you decide how to maximize your benefits.

What is Social Security?

Social Security is a federal benefit program started in 1935 and is a part of the retirement plan of almost every American worker. Each paycheck you receive from your employer typically will have with holdings included. In 2021, 6.2% of your earnings up to $142,800 are withheld for Social Security insurance. Your employer also contributes an amount equivalent to 6.2%. A grand total of 12.4% of your earnings below that threshold amount are paid into the Social Security program. As you contribute to Social Security, you earn credits. You can earn 1 credit per quarter (3 months) you work and you must have earned 40 credits over your life time to qualify for payments from Social Security when you retire. If you stop working before you earn enough credits, the credits will still stay on your account. If you decide to start working again, you can continue to earn credits which will be added to what you earned previously.

The Social Security Administration will calculate what payments you are entitled to receive based on your highest 35 years of earnings, your age, and certain indexing factors and COLA or cost of living adjustments. You can learn more about qualifying and applying for Social Security here.

When can I start collecting Social Security?

If you were born prior to 1955, you are already eligible for full retirement benefits. The Full Retirement Age (FRA), if you were born from 1943 – 1954, is 66. The FRA gradually increases until 1960, at which point the FRA becomes 67 years old. See the chart below.

| Birth Year | Full Retirement Age |

|---|---|

| 1943 – 1954 | 66 |

| 1955 | 66 and 2 months |

| 1956 | 66 and 4 months |

| 1957 | 66 and 6 months |

| 1958 | 66 and 8 months |

| 1959 | 66 and 10 months |

| 1960 and later | 67 |

Early Retirement

You can start getting Social Security retirement benefits when you turn 62. However, your benefits will be reduced compared to those you would receive if you had hit the FRA. Interestingly, according to the Social Security Administration, most people opt to take benefits before reaching their Full Retirement Age, although in recent years the proportion waiting until FRA and beyond has been increasing. Perhaps the reason why is that the reduced benefits you might get when you turn 62 are nearly 30% less that they would be at your full retirement age. This is a substantial amount! Interestingly, the SSA will pay even higher benefits if you can wait a little longer to apply for them.

Delayed Retirement

Working beyond your Full Retirement Age (FRA) has a couple of benefits. First, you can add another year of earnings to your Social Security record. Remember, Social Security looks at the highest 35 years of earnings. Many people make more annually later in their careers than at the beginning. And with the cost of living ever-increasing, adding higher earning years to your SSA record can result in higher payouts. Secondly, your benefit will also increase a certain percentage for each year beyond your full retirement age until you hit age 70. The percentage varies with the year you were born, however, if you were born after 1960, the SSA is projecting that by waiting until you are 70 to claim retirement benefits, you could increase your payment amount to 124% of what you would receive at your full retirement age!

When Should I Retire?

We can’t give you financial advice. Choosing when to retire is a personal decision. No matter what you decide, you should contact Social Security a several months prior to when you think you might want to retire to learn about your options. Talk with your spouse, your family and even a financial planner. Delaying taking benefits even a few months can have quite an impact or your payments through the program.

If you are ready to go, make sure to apply for benefits about four months before you want your them to start. You can find your local Social Security office in our office locator. You can contact the office in a number of ways. Calling your local office will put you in touch will local employees who can answer your questions.

On to the calculators!

It is important to note: These calculators, including those provided by the Social Security Administration itself, can only give you an estimate of your potential retirement benefits. Please uses these calculations wisely.

Retirement Estimator

The Retirement Estimator, provided by the Social Security Administration, uses your actual Social Security earnings record to generate an estimate of benefits for three claiming ages: age 62, the earliest you can claim benefits, your full retirement age (based on when you were born) and age 70, the latest your can elect to receive benefits. The more earnings history you have and the closer to retirement you are, the more accurate this calculator will be.

This is a simple to use but a little clunky. The calculator will ask you your previous year’s earnings and then develop an estimated payout. If you want a little more information, you can click “Get a New Estimate” and then input the age at which you expect to get benefits and the average salary you expect to earn between now and then. This calculator is neutral on when to claim benefits. A draw back, especially for the limited information you get, is that you will have to enter some personal information such as your social security number in to the tool. It uses your identifying information to pull actual numbers from your earnings history. Further, you can only use the tool if you have enough credits to qualify and you aren’t already receiving benefits. Additionally, the pages will time out if you are on them too long without inputting data.

Retirement Calculator

The “MySocialSecurity” Retirement Calculator is a full featured tool that shows you a number of things as well as provides a graph to help visualize the data. You need to create a my Social Security account in order to use this tool. With this calculator, you will automatically be able to see whether you have qualified for Social Security and what your projected monthly benefits for early retirement (Age 62), Full retirement (age 67) and delayed retirement (age 70) will be. You can also make adjustments to the age you want to start receiving payments, the amount of earnings you expect from now until you retire and whether or not to add spouse benefits. This is a very handy tool!

Online Benefits Calculator

You can still benefit from a superior tool, the Online Benefits Calculator provided by the Social Security Administration without needing to create a “my Social Security” or input your Social Security number in an online form. You can manually enter your earnings history, date of birth, desired retirement age, etc to get an estimate of your future Social Security benefit payments . You will need a copy of your Social Security statement to accurately use this tool, however, you could just put estimates in for each earnings year. The less accurate you are with your estimates, the less accurate the calculations will be. It is a hassle to input all of the data, but it is a good option for people who have privacy concerns or are using a public computer and it may take a while to type in each year of earnings.

Planning for Retirement

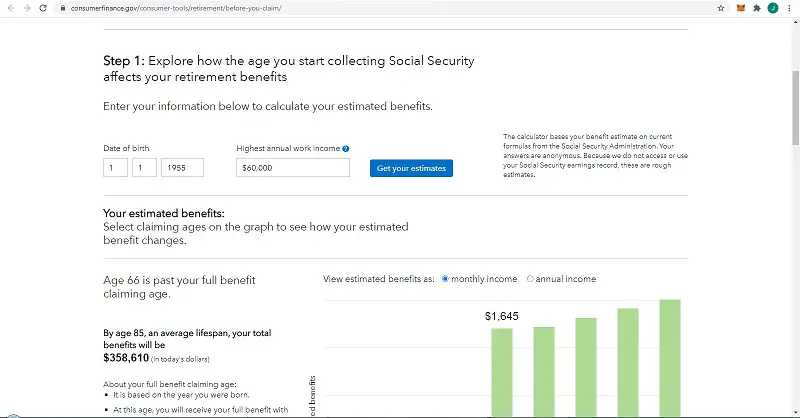

The Consumer Financial Protection Bureau (CFBP) provides a simple, easy to use Planning for Retirement tool. This calculator will give you a general idea of your monthly or annual Social Security benefits. You can input different ages at which you claim Social Security. It provides an intuitive graph. While the Social Security Administration has reviewed the tool and it is provided by a government agency, it does have some weaknesses. The big drawback is that it makes the calculations based on your highest annual income. This is an extremely small and potentially misleading data set. They arrive at their result by doing a a simple calculation based on formulas provided by the SSA. If you have income that varies annually, like a small business owner, or someone in sales, for instance, this calculator may not be the most accurate. But for those pressed for time, it gives a quick glimpse at what you might get and some links to more resources.

Social Security Benefits Calculator

The AARP Social Security Benefits Calculator is a simple to use calculator with a nice interface. You will step through a couple of tabs to arrive a a projected payment benefit. One nice thing is that you can input you and your spouse’s information simultaneously. That said, the big flaw, is that you can only enter in your average annual salary. The calculations are done based on what the SSA provides, however, your average salary might be different than what Social Security will look at for your calculated benefits. For instance, if your salary averaged $40,000 per year over your life time, but your average salary over your highest 35 years of work is $62,000, this calculator might give a much different result than the SSA will.

A nice feature of the tool is the graph that visually shows the effect of your age on when you apply for and receive benefits. It also has a nice calculator to compare your living expenses with your Social Security benefit. It also has a tab that will show you what happens when you receive benefits and keep working. All in all, a very nice tool!

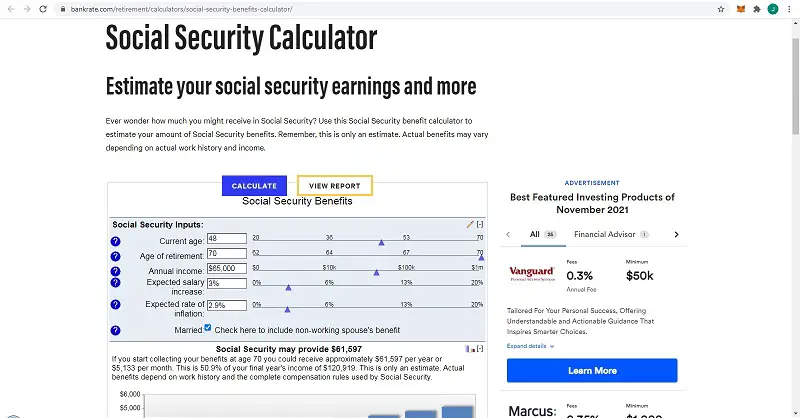

Social Security Calculator

In just 5 or so form fields, Bankrate’s Social Security Calculator tries to provides a rapid estimate of what you might expect your future Social Security benefits to be. Like the other non-SSA calculators, your benefits are based on your future earnings input and some assumptions. It has a nice graphical output that shows the increase in your payments as you delay receiving benefits. It also allows you to adjust for earnings growth and inflation, which will affect your anticipated payments for Social Security. you can also create a report in one click which you can print out and keep for your records.

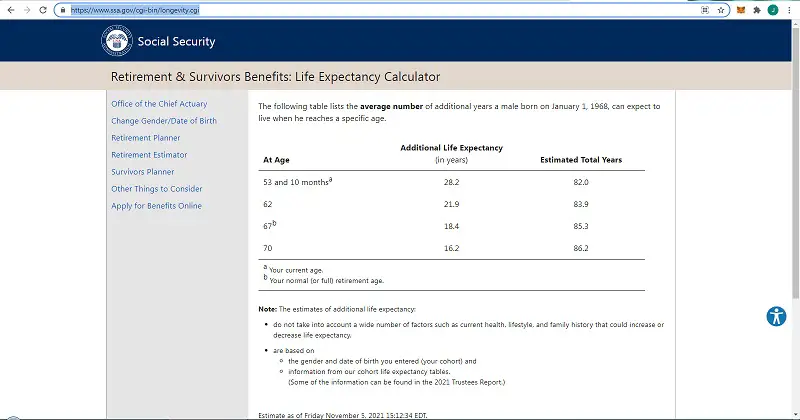

Life Expectancy Calculator

Let’s be honest, figuring out the best time to start taking Social Security benefits involves several factors, including how long you are going to live. Obviously, we don’t know what tomorrow will bring, but the SSA has provided a Life Expectancy Calculator that will help you determine the average number of years left a person of your age and sex has left. It won’t take into account your current health, how much you exercise, what you eat, or your genetic makeup and family history. It is a little morbid, I know. But, because your spouse can receive survivor benefits based on the amount you were entitled to, it makes sense to take this into account when retirement planning. If you want to see a more complete estimated life expectancy calculator, check this one out.

Let me again just say that these calculators, even the ones from the Social Security Administration can only provide you an estimate of what you might receive as payments when you retire. You actual benefit will vary based on the accuracy of the data you input in to the tools, variability on your earnings, legislative and administrative changes, inflation adjustments, etc. Use them wisely.